Gunnar Fairbairn

Ralph Drayton

Economics

12th November

2016

Interview Answers

1. Sam, 71, male.

2. Live in own home

3. BA History, MFA English

5. 85,000 (Retirement, Social Security, Mandatory Distributions)

6. Wage is basically reasonable

7. Middle class

8. About the same. They both worked and had the benefits of

belonging to unions.

9. Delay in buying first house. No help from family getting a down

payment, and timing delay was several years that peer group proved to do much

better by starting earlier.

10. Govt. was helpful in forgiving educational loans in exchange

for teaching.

11. Dreams and fears of the economy have had little to do with

things.

12. Yes

13. The moment you receive your first paycheck, pay yourself first:

15%. Do this every month. Your employer may make this convenient by

offering a 401K. If you save your money each month and don't have a 401K

start purchasing a small piece or real estate, a lot, an acre of farmable land,

something you can get $ from, by renting it to a goat, or whatever, even a

small house. Do this early in your adulthood. Don't make excuses

about $$$.

Intellectuals Succeed: An Economic

Profile of a Teacher & Former Stock Broker

Retired Decently

I interviewed a retired man in his

early seventies and found that thanks to a few personal finance decisions made

early on he now enjoys a comfortable retirement. In no way was he rich, but he

thought ahead from the time he went to college. Upon examining what he

attributes to his success, such as personal finance forethought, union

pensions, and education its easy to see how he came to financially healthy

retirement. I intend to examine those decisions and apply some of what I’ve

learned in economics this year in reflecting on his economic profile.

Though he says he was lucky for the government forgiving his student debt in exchange for teaching I think his academic boldness was bound to put him on better financial footing than most people. In 1950’s it wasn’t a requirement to go to college and college educated workers didn’t make substantially more money. He went though and got a BA History, MFA English, which added a ton to his human capital in the labor force.

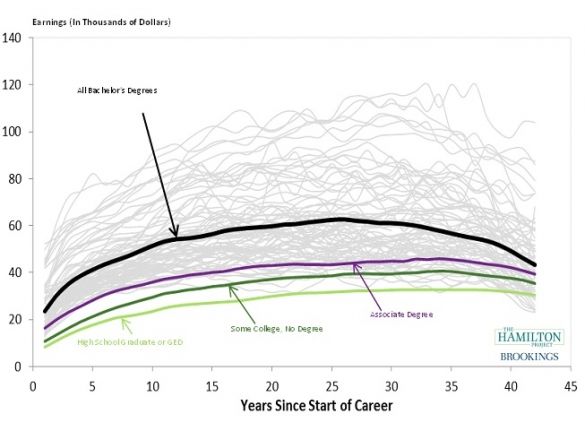

Though a bit blurry this chart shows

lifetime incomes of those with a bachelor’s degree, high school diploma, some

college, associates degree, and above. With a bachelors and a masters, he stood

in the best position to have the highest possible life income on average.

Getting a masters was risky in terms of student loan debt, but the amount of

people going to college before the 1950’s was much lower. Also less money was

being spent on renovating them for a growing student base making Sam’s

education much cheaper with inflation adjusted numbers. The federal government

also forgave that debt in exchange for teaching. That’s a very good deal.

Race, gender, and class is another

factor in dealing with the cost of raising a family and one’s general overall

income. In class we discussed systemic poverty once and I don’t think there was

any danger of him falling into that cycle. He started out middle class and

prepared for upper middle class with education and considers himself middle

class now. He is white and male and predominantly men like him get paid more than

black male counter parts. Though the gaps are well exposed now, the race and

gender gaps played to his favor back in the 1970’s and for the majority of his

working life. Today 73% of white families own homes compared 45% to 47% for

Blacks and Latinos. Owning a home is great investment because with the rise of

inflation overtime you end up paying less then what you bought the home for in

some cases. Inflation rises devaluing your debt, but raising the value of your

home. Buying that first home was a bit of struggle he remarked in the interview,

but he eventually did get one as he says here “Delay in buying first house. No help from family getting a down

payment, and timing delay was several years that peer group proved to do much

better by starting earlier.” It seems here he missed out a bit financially

among his peers, but he was still able to the make investment, which most

definitively benefited him in the long run because he owns his home today.

With the background of

an academic and several profitable careers behind him his retirement pay had to

at least be “reasonable” as he puts it. He now makes about 80,000 a year in

retirement, which is above the national average income of 51,000 a year and

certainly more than minimum wage. His advice out of this interview is advice my

parents also have given me.

“The moment you receive

your first paycheck, pay yourself first: 15%. Do this every month.

Your employer may make this convenient by offering a 401K. If you

save your money each month and don't have a 401K start purchasing a small piece

or real estate, a lot, an acre of farmable land, something you can get $ from,

by renting it to a goat, or whatever, even a small house. Do this early

in your adulthood. Don't make excuses about $$$.”

Under the belief of

dollar cost averaging the first part makes a lot of sense. Investments will

grow over time and continuous investment results in more invested when it is

cheap then its expensive. A 401k would balance his income in stock and bonds

and the stock would provide a nice profit with consistent investment that

usually yields higher returns due to people buying more when a stock is low and

less when a stock is high. He seems to also be ahead of the trend when it comes

to saving for ones retirement not through a home, but through a bank account.

Assuming these retirement accounts are managed by big corporations

whatever they invest in his bound to grow just due to the size of the overall

principle. Meredith mentioned that a large portion some estimates being 40% of

the stock market is invested in funds, money managers, and overall passive

investing. Considering this and how volatile the stock market growth is today

compared to when my grandfather was investing I’ve generally come to the belief

that where these passive investors and money managers see value other should

join the bandwagon because they bring a sizable investment principle with them

and may just dictate the market.

Some questions I have

from this interview still are why did he get that masters in fine arts with

little economic pressure fifty years ago? As a former stock broker how does he

see the market today? How did the opening up of the investment world to more

people effect the market in his view? Does he worry about wage slowing, but

stock market gains rising?

All images had to go to the bottom of the page due to posting issues.

Cited Sources

http://apsforupte.org/upte-on-the-issues/fair-compensation/

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.