http://www.bernardwolf.com/media/original/CityscapeLA-copy-DUP.jpg

K.C. was born in

a rural southern Indian village in 1937. Unlike his other siblings, he sought

to leave India for greater economic opportunity. For him, immigrating would

have to be through education, specifically through engineering. Completing high

school, and undergraduate studies in India, K.C. was granted the opportunity to

receive a Master’s in Engineering at Oklahoma State University. In 1965, once

out of graduate school, K.C. attained a job in San Francisco, California,

working as a Construction Engineer at Fred Early Construction. Three years

later he was promoted to Construction Project Manager within Fred Early. While

in San Francisco, K.C. bought his first house, in the suburbs, and got married.

In 1970, in San Francisco, K.C. began work with a larger construction company,

Dillingham. Working as a Project Manager, K.C. eventually was asked to

transition to Los Angeles, California to continue his work. When in Los

Angeles, K.C. had two daughters, and lived in a wealthy Los Angeles

neighborhood, in which he moved houses four times. K.C. continued to elevate up

the corporate ladder, attaining the title of Vice President, and eventually

Executive Vice President for Dillingham. A decade after obtaining the promotion,

K.C. was asked to become President of Ray Wilson Construction, where he worked

for 13 years, earning his highest salary, $275,000. In 1998, after leaving Ray

Wilson, K.C. became a consultant for several Los Angeles-based construction

firms. After officially retiring in 2005, K.C. moved to Portland, Oregon, to

surround himself with his daughters, and his grandchildren. Currently, on an

annual basis, K.C.’s retirement income is $120,000.

Assessing K.C.’s

life through the principles of the economic perspective, it becomes evident

that parallels emerge. With the economic belief that “institutions are the

rules of the game,” it’s apparent that K.C.’s economic success, is a product of

institutions. Beginning with the structure of education, K.C. was able to work

hard throughout high school and undergraduate studies, which allowed him to

received his Master’s in the United States. The institution of education, “was

a key determinant of my success,” stated K.C. Furthermore, the fifth principle,

“all choices have consequences that lie in the future and reshape what’s

possible,” applies to K.C., as his decision to dedicate his youth years to

academics, allowed for him to immigrate to America. His move to the United

States forever changed in his economic standing. “If I had stayed in India, I

would’ve worked in the fields and continued my life as a villager,” stated K.C.

His decision to use education as a means of expanding his opportunities, had a

profound impact on his economic well-being.

Much of K.C.’s

economic success, is attributed to his ability to escalate through the

corporate ladder. Beginning with his first job in San Francisco, K.C. was able

to secure a “strong wage,” due to his Master’s in Engineering. His depth of

study in the field of engineering directly boosted K.C.’s human capital. As a

master in his field, K.C. was of higher demand, and was immediately able to

ascend to, what he called, “an above entry level position,” as a Construction

Engineer. By starting at a higher position than most first-time workers, K.C.

was able to accelerate his way through Fred Early Construction. Additionally,

by quickly moving up to an executive position within Fred Early, K.C. became a

viable prospect to move into an executive position within a larger construction

company. The wealth of experience K.C. attained at Fred Early, built upon his

human capital. With each promotion K.C.’s services become more demanded.

Throughout his ascension, and ultimate arrival as the President of Ray Wilson

Construction, K.C. cited a growing demand for construction. Beginning in the

1970s, according to K.C., malls, and mass retailers became growingly popular.

The rise of the mall, meant a heightened demand for corporate construction. The

growing demand for construction, meant a growth of construction companies.

There is an apparent connection to the supply-demand curve: as demand for

construction increased, so did the size of construction companies. As construction

companies grew, Project Managers, like K.C., became more integral, and were

handsomely compensated. K.C. attributed his rising wages to scarcity. As he

gained more experience, people with K.C.’s repertoire became increasingly

numbered. Simply said, K.C.’s wages and human capital shared a linear

relationship: his wages increased at each level he was promoted. K.C. discussed

the role of taxation in his life, claiming, “Taxation didn’t significantly

alter my wealth, and I often felt that I was doing justice by putting money

back into the system.” Over the course of his professional, and retire life,

K.C. was assigned a exceedingly livable wage reflective of his human capital.

Throughout

K.C.’s professional life he experienced several recessions. As a member of the

workforce, he, firsthand, saw the business cycle playout. During the recessions

of the1970s, and early 1990s, K.C.’s construction companies saw significant

dips in clients, and often had to lay off lower-level employees, in order to

remain cash flow positive. However,

after recessions, K.C.’s companies would often experience periods of expansion,

in which their client list, number of employees, and wages would all increase.

The expansion was often catalyzed by the Federal Reserve’s lowering of interest

rates, which subsequently lowered the interest rates of commercial banks,

allowing companies, including K.C.’s constructions company, to borrow more. The

ability to borrow at a greater degree, had a multiplying effect, as more people

were hired by K.C.’s company, lowering unemployment, resulting in the expansion

of the consumer base.

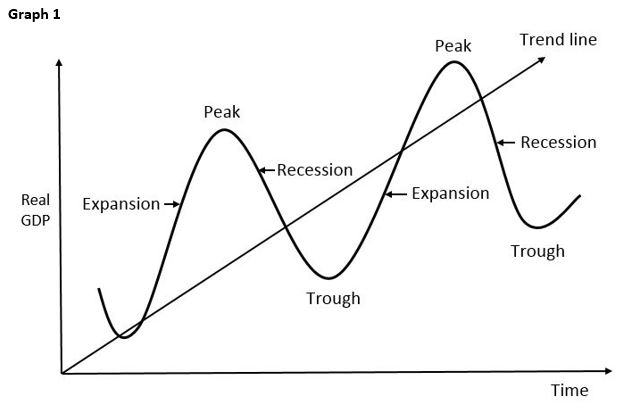

The trends

expressed in K.C.’s companies were emblematic of the Phillip’s Curve, in which

unemployment and interest rates share an inverse relationship. During periods

of recession, as in the 1970s and 1990s, more people are unemployed, so the

Federal Reserve lowers interest rates, allowing companies to borrow more and

expand their firm, hence combatting mass unemployment.

The Phillip’s Curve

Another means to

which K.C. gained greater economic security was through investing. K.C.,

beginning with his first job, was able to make enough money to the point that

he could begin both saving and investing. K.C. throughout his life made it a

point to invest, as a means to actively expand his capital. However, he stated,

“I’m a risk-averse investor.” He elected to invest in companies with large

market caps, as larger market caps were symbols of stability. K.C. also

addressed taxes on capital gains, stating, “Similarly to Federal taxes, I felt

that my capital gains were taxed fairly. He recommended that younger people

follow his method of investing, due to the consistent, albeit relatively low,

returns. However, K.C. unlike many, was able to grow his wealth at an

exponential rate, due to the sheer amount of liquidity he had. With high-wage

jobs, K.C. was able to invest more, than the average-wage worker. K.C.’s story

of investing is reflective of Thomas Piketty’s idea that the wealthy get

wealthier, due to their ability to invest. K.C. had the luxury of being able to

invest starting at a younger age, which allowed him to have substantive amounts

of capital once retired.

Throughout my

interview with K.C., two interesting themes emerged: education and perspective

When interviewing K.C., it became clear that education plays a significant role

in future earnings, and the opening of opportunities. K.C.’s in-depth study in

engineering was integral in attaining economic security. Had K.C. chosen to not

study engineering, he would’ve never have had the opportunity to achieve the

same financial success, let alone immigrate. Yet, by far the most interesting

point K.C. made in the interview addressed the perspective of wealth. When

living in India, K.C.’s family was considered upper-middle class. And when I

asked K.C. what socioeconomic class he felt a part of, he stated, “upper-middle

class.” K.C. laughed when stating that, as there is a significant disparity

between upper-middle class in India, and in the United States. Upper-middle

class in India, for K.C., meant property ownership, whereas in the United

States, upper-middle class, in regard to K.C., meant having copious amounts of

liquidity. The dichotomy highlighted by K.C. suggests that economic terms and identifiers

are relative to their environments. A lack of proper global perspective when

assessing an individual’s economic story can have significant implications

regarding the interpretation of material. For example, had I not learned the

true meaning of upper-middle class in India, I would’ve assumed that the characteristics

of upper-middle class in the United States were identical to those in India.

Overall, the

opportunity to interview a retired immigrant, provided an intriguing insight

into how I want to live my own life economically. K.C. encouraged me to start

saving and investing capital as soon as possible, in order to obtain future

financial security. Yet, what I learned, from K.C., the value of pursuing

opportunities both big and small. K.C. remarked, “Had I not taken the

opportunity to move to the United States, I would’ve followed the footsteps of

my family, remaining a villager.” The global economy is built on individuals,

firms, organizations, and countries making choices. And much like the global

economy, K.C.’s economic life story was heavily dependent on his ability to

make decisions.

){kind=link}

){kind=link}